Introduction & Preface | Chapter 1 | Chapter 2 | Chapter 3 | Chapter 4 | Chapter 5 | Chapter 6 | Chapter 7

Translator’s note:

As a former student of Anwar Shaikh, “equilibrium” and “perfect competition” evoke for me the worst of mainstream economic theory: preposterous assumptions (perfect knowledge, price-taking firms, perfect mobility and substitutability of factors, etc.) and a dehumanizing mechanistic logic of operations. Much of Shaikh’s magnum opus – Capitalism: Competition, Conflict, Crises (Oxford 2016) – is an exhaustive take-down of these theories. So, when I first read this short chapter, in which Luis Razeto summarizes equilibrium, marginal cost, average cost, marginal revenue, and perfect (and imperfect) competition as commonly understood, I had to remind myself to say “yes” twice to the text.1 Of course, Razeto is not simply repeating the standard economic formulas, instead he is carefully setting the stage for an analysis of cooperative business operations that will enable us to continue drawing clear lines of demarcation between capitalist firms and cooperatives, with important theoretical and especially practical implications. As we have seen in previous chapters, Razeto’s approach is to “empty and re-fill” concepts from mainstream economic theory – e.g., factors of production, property, surplus and profit, accumulation – using them to lay out a broader theory that does not presume capitalist relations of production and its operational logic.

I have placed the two simple graphs presented in this chapter in the Appendix.

- Matt Noyes

SECTION TWO

THE OPERATIONAL LOGIC OF WORKER AND COMMUNITY ENTERPRISES

Chapter 8

On Equilibrium and Profit Maximization in Cooperatives and Capitalist Enterprises

1. Having analyzed the essential differences and specific structural problems of cooperatives organized by Labor and Community in Section One, we now turn our attention to their operational logics and economic efficiencies.

The central question we will address in this Section is the one that economic theory has defined as the problem of the equilibrium of the firm. As each type of enterprise has a particular functional or operational economic logic, and specific constitutive relations, our analysis will have to differentiate among the various ways the problem of equilibrium is posed.

To define the equilibrium of the firm one must first identify the conditions under which the economic unit obtains the maximum benefit from its activities. These conditions, in turn, determine the optimal expansion of productive forces, that is, the point at which the enterprise is the right size for the market in which it can operate. So, the question of equilibrium is posed in terms of an objective to be achieved through a process, and to answer it, one must identify the best strategy for growth, based on the available resources and the given market conditions.

The key questions, for any type of enterprise, are:

-

What level of production will generate the greatest gains for the enterprise?

-

What is the best and most economical combination of production factors in view of achieving the desired volume of production and profits?

The general concepts and criteria that economic theory has elaborated to answer these questions are based on the specific experience and operational logic of capitalist enterprises. The resulting abstract model of behavior assumes that the firm has an infinite range of possible combinations of factors (“full substitutability”), and that it operates in the context of a competitive market (both for factors and products). These assumptions enable one to simplify the problem analytically, which does not invalidate the theory as such, but does limit its theoretical significance and its practical applicability. Successive elaborations have improved on the initial model, introducing more realistic and complex analyses regarding the margins of adaptability in an enterprise and the limits to free competition in a given market.

Any theory of equilibrium that claims to have general validity (if only for one type of enterprise) necessarily involves analytical abstraction and simplification of the problem on which the model is based. Our analysis of equilibrium in cooperative enterprises shares these characteristics and limitations. But, the mechanical application to cooperative enterprises of a model for equilibrium developed for capitalist firms would not be a legitimate abstraction but simply an unjustified generalization.

To understand the problem of equilibrium in enterprises organized by Labor, and how it differs from that which applies to capitalist enterprises, it is opportune to start with a consideration of the model that economic theory has constructed for the latter. Various concepts and considerations developed for this type of enterprise will still be useful to us in relation to our particular subject.

Generally speaking, the term “equilibrium” signifies a balance of two forces or variables. In economic theory, equilibrium is the point at which there are no incentives for the agents involved to modify their behavior. In microeconomics, an economic agent (a firm) is said to be in equilibrium when, given certain variables outside of their control, any change that the agent could make to balance among variables would worsen their situation.

When one speaks of the “equilibrium of a firm,” the goal and rationale of the economic agents involved is the maximization of the profits of the enterprise; thus, a firm is said to be at equilibrium when the variables under its control are balanced at a level that permits its maximum profit. More specifically, the level of production that permits maximum profit is based on a balance between supply and demand reflecting the costs of production and the market prices of products (assuming the optimal combination of factors used for each level of production). In seeking the “equilibrium” volume of production in a capitalist firm it is obvious that it is a matter of identifying – and practically achieving – that level of production in which the difference between the total revenues and total costs is at its greatest.

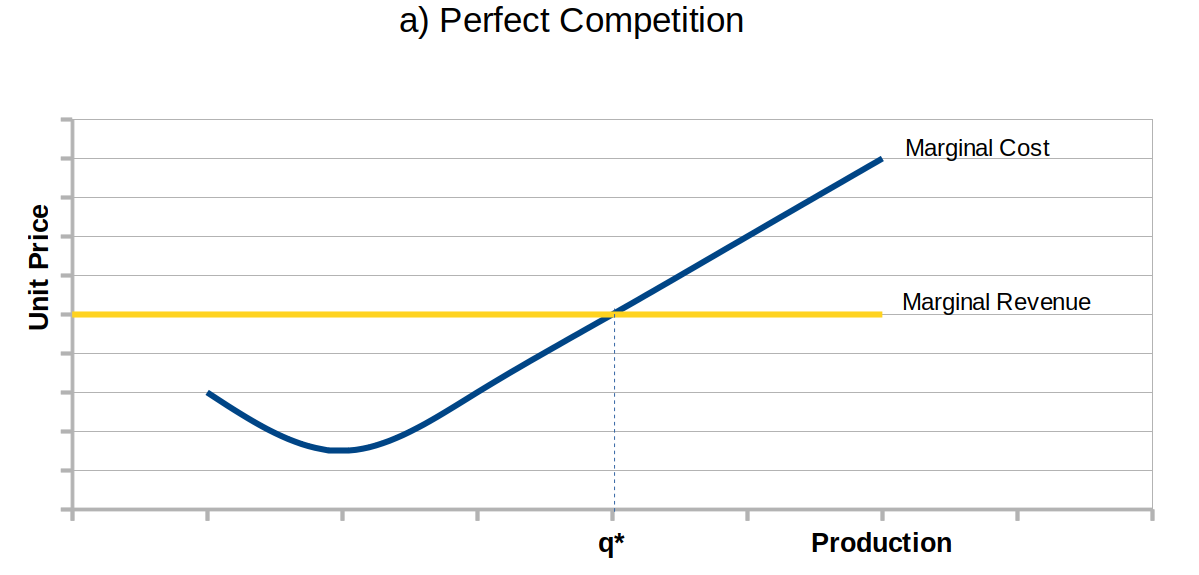

We know that, for the firm, any increase in the quantity of products implies greater production costs, which means that increasing total production by unit has a specific marginal cost. At a level of production that is very low in relation to the available productive capacity, the marginal cost can decline as the quantity of products in increased; while this happens we can say that the enterprise is producing at an uneconomic level. But at a certain point – which we can consider the minimum level of exploitation – the material costs begin to grow as the enterprise grows. Thus, the firm will reach a level of production at which it will obtain the greatest profits and beyond which it should not increase production.

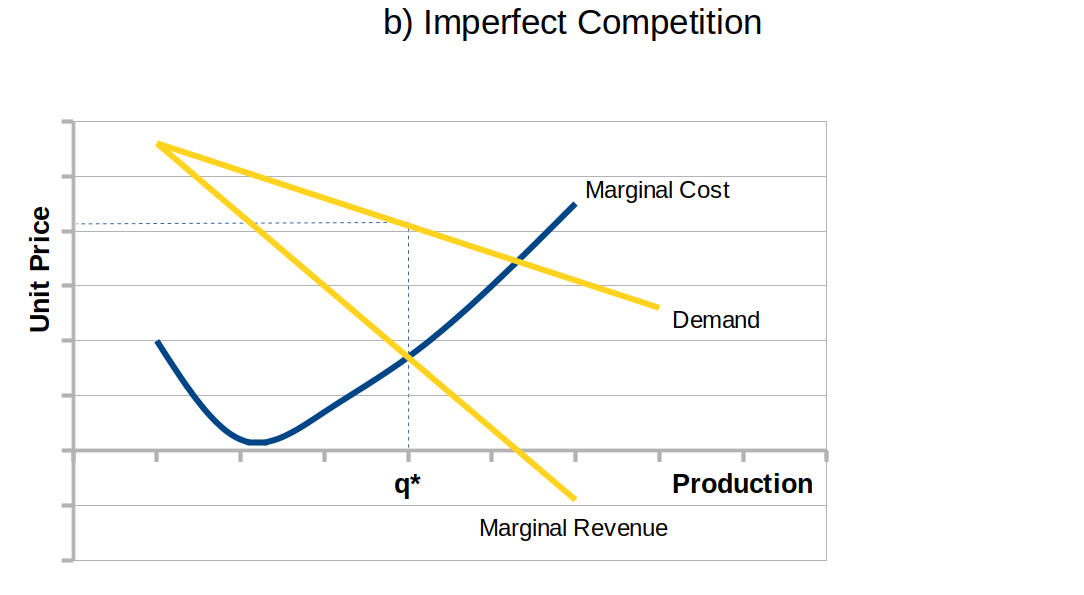

On the other hand, the increase in production (and sales) signifies an increase in total revenues, that is, for each additional unit of product sold there is a specific marginal revenue. In the case of perfect competition this marginal revenue will be constant (and equal to the price), because it is assumed that the supply of any individual enterprise is not sufficient to affect the market price. In the absence of perfect competition, in order to increase sales, the enterprise should accept a lower price per unit, resulting in a marginal revenue that is lower than the price, and declining.

This being the case, the enterprise should raise its production to the point at which the marginal cost (the cost of production implied by an additional unit of product) is equal to the marginal revenue. The difference between total revenues and total costs is greatest at this point, which is the point of equilibrium for the firm, that is, the point at which it will obtain maximum profit. In effect, whether the firm produces less or more, the difference between revenues and costs will be reduced: in the first case it will be losing the marginal gains on the units it does not produce, and in the second case, the cost of raising production will be greater than the revenue that could be obtained.2

As we have indicated, this theoretical model of equilibrium of the firm has been questioned insofar as it does not take into account the real market conditions in which enterprises have to operate nor other specific problems that arise in the course of increasing production. But even if alternative theories and models are advanced in the debate, the effective result has been a progressive enrichment of the theory of the firm that rather than invalidating it has corrected, improving on its original elaboration.

A first improvement has been an important distinction between short and long term equilibrium, arising from the recognition that as the firm grows, the average unit cost of production declines due to internal and external economies of scale. Nonetheless, this decline has a limit. Once the firm reaches a certain size it begins to successively raise its costs generating a declining curve in economies of scale or producing diseconomies of scale; this because of greater bureaucratic costs, loss of flexibility in the market, conservative policies with regard to risk, etc. The average cost curve adopts the U form, which modifies in consequence the shape of the marginal cost curve. Thus, the enterprise will have reached its optimal size (minimum efficient scale) in the moment at which the average cost and marginal cost are equal.

Now, if the market price for products is higher than the point at which the average cost equals the marginal cost, the firm will receive excess profits, a situation which, in conditions of perfect competition, can not be maintained as new firms and investments will be attracted to the sector and the product price will fall. In such conditions, a new long term equilibrium will be achieved, given the equivalence of the average cost, the marginal cost and the unit price of production. Such a long term equilibrium point has been called the technical optimum (óptimo técnico).

Equilibrium theory has also been criticized on the grounds that because the market does not operate in conditions of perfect competition, there is no reason to imagine that its free play will naturally lead enterprises to their technical optimum. However, this critique only invalidates the thesis that the market, by itself, guarantees the optimal assignment of resources. That is, it is a critique of the macroeconomic theory involved, and does not completely invalidate the model’s microeconomic theory, inasmuch as the general criterion proposed for understanding the behavior of the firm remains (more or less) sufficient. In the first place, the rule of maximization is unchanged, that is, the equilibrium level of production continues to be that at which the marginal cost is equal to marginal income, whether competition is perfect or imperfect. In the second place, the fact that equilibrium is never reached at the macro level does not negate the fact that the firm will likely be guided in its decisions by the search for its particular technical optimum: it will continue growing as long as the market prices assure it extraordinary profits, and it can be considered to have reached its adequate size if the price it obtains for its products begins to be inferior to the point at which its average cost and marginal cost curves cross. A firm that desires to continue growing should proceed by diversifying its production, introducing technical changes to the product, new marketing strategies, etc.

One important correction to the theory of equilibrium that has been proposed is based on considering the market, demand, and prices not as a given conditions but as a field of operations in which the firm’s decisions have relevant effects. When firms make decisions, they take into account the decisions of other firms, which do the same in return, in an active process of struggle for market share and access to the other factors. The price curve takes variable contours, and, being a variable partially dependent on business decisions, the point of equilibrium and the technical optimum can be established at more than one level or place; which is to say the enterprise has more alternatives than simply the optimization of profits and the optimal scale of operations.

Moreover, if demand is not perfectly elastic (perfect elasticity means the price does not vary with changes in the level of production) and has a limited volume, and if the prices are not given by perfect competition but are shaped by situations of monopoly, by variations in the costs of production, management decisions with regard to risk, lack of information on the part of consumers, etc., firms will be forced to carve out their own spheres of demand on the basis of strategies which may imply a greater or lesser departure from the equilibrium point and the technical optimum.

In certain contexts, the firm might consider marginal costs above or below the average cost to be acceptable. Depending on the situation, they might even accept average costs that are higher than prices, which would imply working at a loss. Still, the firm should always operate around and seek to achieve these levels of maximum profits, given a specific period of time within which it expects its investments to pay off.

In other words, the economic struggle conducted in the market through demand and prices can not deploy itself in an arbitrary form, but in relation to certain “laws” of economics that leave room for choice among various reasonable strategies.

The discussion and theoretical development of these problems does not end here, of course, and is obviously much more complex. Another line of improvement of equilibrium theory addresses the consequences of operating in market conditions of imperfect competition that is “oligopolistic,” that is, in which demand is more elastic in cases of price increases and less so in cases of decreases.

In oligopolistic conditions, the price of products tends to stay stable due to a kind of tacit accord between producers, for each of whom it would seem acceptable to operate at whatever level falls between these two hypothetical situations, a) marginal cost below marginal profit, which supposes a higher price, and b) marginal cost higher than marginal profit, which would suppose a lower price. Once the price has been fixed at an acceptable level for all the employers, it tends to stay stable until the costs of production changes homogeneously for all firms. This being the case, no firm can raise its profits by competing with the others; as a result the market imposes on all of them a certain level of common or “normal” profit.

Another line of improvement of the model of equilibrium arises from this reality: considering as an immediate criterion for decisions under conditions of oligopoly not the maximization of profits but market share. For a firm operating at a fixed rate of profit (10% of the total cost, for example) the objective becomes broadening the proportion of total demand it meets. As it is a matter of a rate of profits, it is obvious that an increase in market share raises the sum of total profits as the firm sells more. The theory of market share does not contradict the general principle that establishes the maximization of profits as an objective of the enterprise in the medium and long term. What does constitute an important alteration is the consideration of total cost and not marginal cost, and treating average cost per unit per of production as a variable to be taken into account in the determination of prices and equilibrium.

What matters here is less a question of theoretical implications than practical use: the use made of the model by a firm’s directors. In planning production, they take into account the fact that the quantity produced is never a constant, since sales fluctuate seasonally and cyclically. The target quantity is an estimated average, something less than the maximum that could be produced given the available facilities, technology, and labor force. Any increase in sales over this average, that is, any tendency toward a larger presence in, and control over, the market is seen as a source of extraordinary profits.

We now leave this somewhat rushed synthesis of the theory of the firm and its development, elaborated on the basis of the specific logic of capitalist firms. The intention of this brief overview was to introduce the reader to the concepts of equilibrium, growth, and the technical optimum, all of which require an alternative theoretical treatment if they are to be useful to us as theorists and practitioners in cooperative enterprises and worker cooperatives.

2. In order to build an alternative perception from the ground up, one that we can consider intuitive in that it presents both the familiar capitalist model and some cooperative alternatives, it is useful to observe concretely what it is that the capitalist entrepreneur is doing when they evaluate projects and make decisions about levels of production, costs, prices, etc., in pursuit of the goals that are suggested by economic theory. Of course, in any enterprise, the internal and external factors of production need to be combined in the right proportions; decisions must be made about technology, administration and management, labor, finance, publicity, investment, purchase of inputs, sales, inventories, etc. But in the enterprise organized by capital all of these questions are translated concretely into decisions about how to apportion the finance factor. The firm’s strategy for achieving equilibrium is composed principally of decisions related to the utilization of the money they have invested, as well as the external financing to which they may have access. In other words, the goal is to make the most objective decisions possible about the uses of “things” (factors and goods) as monetarily quantified.

For the worker cooperative enterprise, the factors have an essential and inseparable subjective dimension: they are all in some way the work of the workers themselves. The questions about how to apportion technology, administration, labor, investment, and other factors all affect the workers directly or indirectly as the subjects who make the decisions and are responsible for them. The strategy of the worker enterprise is composed principally of decisions relative to the self-exploitation or utilization of their own labor power (previous, current, or future), and that in relation to the workers’ own present and future needs.

APPENDIX

Citations

Luis Razeto Migliaro, Matt Noyes (2023). Cooperative Enterprise and Market Economy: Chapter 8. Grassroots Economic Organizing (GEO). https://geo.coop/articles/cooperative-enterprise-and-market-economy-chapter-8

Add new comment